Stripe's $1.1B bet on Bridge - Why every fintech needs a stablecoin strategy

How Programmable Money, AI, and Blockchain are reshaping payments, banking, and financial Infrastructure

The financial system is evolving, and stablecoins are at the centre of this transformation.

Despite a tainted start, blockchain technology is now rapidly becoming the backbone of global digital payments, adopted by fintechs and merchants.

Stripe’s $1.1B acquisition of Bridge is a clear signal that stablecoins aren’t just a niche product: they’re a key part of tomorrow’s financial infrastructure.

In this article, we’ll cover:

🪙 Why stablecoins are on the rise - and what that means for fintechs.

➡️ How Stripe’s acquisition of Bridge is accelerating the adoption of stablecoin payments.

🔎 The businesses already using stablecoins today (Starlink, PayPal, Klarna, Robinhood).

📱 Why stablecoins are a game-changer for cross-border payments, BNPL, and payroll.

🖼️ The regulatory landscape, and why Trump’s new executive order matters.

✨ The biggest opportunities for fintechs, digital banks, and developers in this new financial era.

If you follow me on LinkedIn, you might have seen my recent post about Stripe’s massive $1.1B acquisition of Bridge.

Interestingly, just a week before this news, I wrote Money 2.0: How Programmable Money is Transforming Finance, where I broke down the shift from Money 1.0 to Money 2.0. No jargon, just simple explanations.

The two key ingredients of money 2.0

1️⃣ Programmability - Making money smarter by enabling conditions for its release.

2️⃣ Interoperability - Simplifying global money exchange, making transactions seamless across borders.

With Stripe’s latest move, it’s clear that Money 2.0 is accelerating fast, bringing us closer to a world where money isn’t just digital, but programmable and globally connected.

Stablecoins are on the rise 🚀

The digital currency USDC (a stablecoin issued by Circle) has quickly become a major player, experiencing phenomenal growth with:

✔️ $1 trillion in monthly transaction volume

Its stability (1 USDC = 1 USD) and global availability through wallet apps like Coinbase, making it a trusted digital dollar for cross-border transactions.

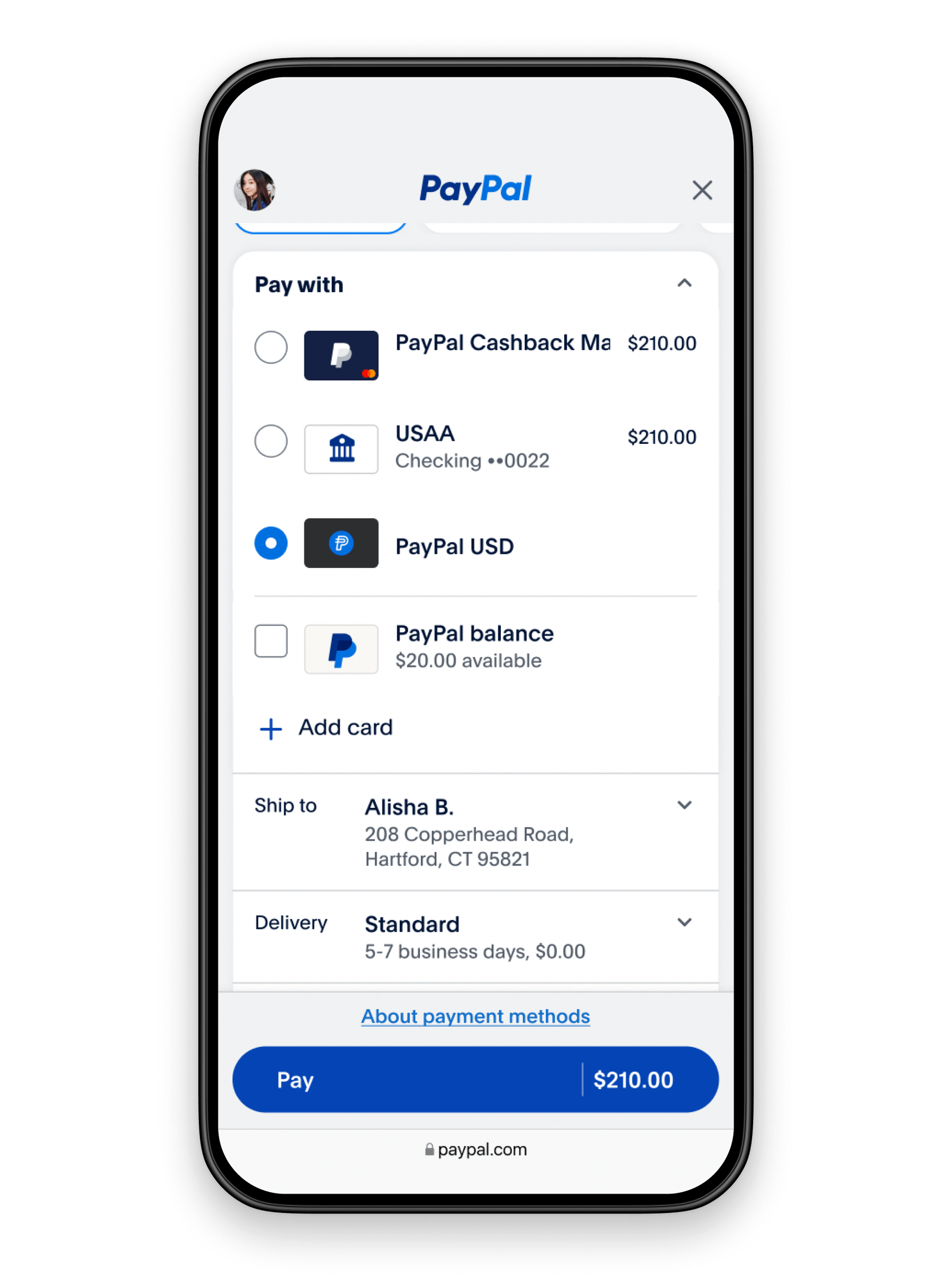

Platform-based stablecoins: Paypal’s PYUSD

USDC’s popularity has paved the way for new stablecoins, including PayPal’s PYUSD (PayPal USD). With 432 million customers, PayPal’s move brings faster, cheaper transactions to its existing audience, allowing their users to move money globally with lower fees.

💳 Ecommerce adoption is next, as more consumers use stablecoins, merchants (including those using PayPal) can now accept them at checkout, unlocking a new era of digital payments.

PayPal isn’t alone in enabling stablecoin payments. A few months back, we covered Triple-A, which has helped global eCommerce businesses like Farfetch accept digital currencies at checkout.

Starlink: A global business using USDC for payments

Companies like SpaceX’s Starlink have already embraced USDC as a global payment method.

Starlink’s mission is global, decentralised, and futuristic - bringing high-speed internet to every corner of the planet and disrupting traditional broadband infrastructure.

While regulatory requirements still apply in each country, Starlink is making significant progress, expanding to remote and underserved regions where banking access is often limited.

Why Stablecoins make sense for starlink

✔️ Borderless transactions – No reliance on traditional banking infrastructure.

✔️ Lower fees – Avoids high international payment costs.

✔️ Instant payments – Seamless global access for customers.

As of now, Starlink operates in 100+ countries & territories - and offering stablecoin payments is a natural fit for a company that’s already breaking barriers in connectivity.

Stablecoins x BNPL?

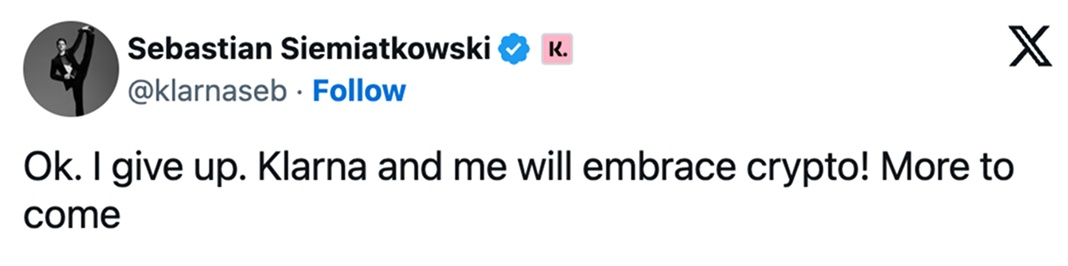

Recently, Klarna’s CEO, Sebastian Siemiatkowski, hinted at a new strategy involving stablecoins, just ahead of their upcoming IPO.

With 150 million customers across 26 countries, Klarna’s potential move into stablecoins and blockchain-based finance could unlock major advantages for the leading BNPL provider, including the ability to tap into DeFi (decentralised finance) for lending and liquidity solutions.

What’s interesting is how much Sebastian Siemiatkowski’s stance has shifted. Just three years ago, he dismissed crypto as a “decentralised Ponzi scheme.” But recently, he acknowledged his change of heart on X, posting:

“Sometimes you’re wrong.”

Robinhood use stablecoins for 24/7 settlements

This week, Vlad Tenev, CEO of Robinhood, announced that the company is now using stablecoins to solve a long-standing issue in finance: banks’ limited working hours affecting settlement times.

Traditional banking systems operate on fixed hours, leading to delays in processing transactions, especially on weekends. By integrating stablecoins, Robinhood can now facilitate instant, 24/7 settlements, eliminating downtime caused by legacy financial rails.

“We’re using stablecoins to power a lot of our weekend settlements now, and we’re using it increasingly.”

Vlad Tenev - Robinhood CEO

With real-time, borderless transactions, stablecoins are quietly transforming fintech and Robinhood’s move is another step towards a truly always-on financial system.

Trump embraces Stablecoins

US President Donald Trump has signed an executive order titled “Strengthening American Leadership in Digital Financial Technology,” which explicitly supports dollar-backed stablecoins and prohibits the development of a U.S. central bank digital currency (CBDC).

This move aims to promote innovation and financial autonomy while reinforcing the U.S. dollar’s dominance in the digital economy.

In line with this strategy, Trump has nominated Brian Quintenz, the former head of policy at a16z crypto and a previous commissioner of the Commodity Futures Trading Commission (CFTC), to lead the CFTC.

Quintenz is known for his advocacy of blockchain innovation and is expected to play a pivotal role in shaping the regulatory landscape for digital assets.

➡️ Why this matters:

It legitimise stablecoins: by providing official support for dollar-backed stablecoins, offering regulatory clarity and encouraging their adoption in the U.S. financial system.

Better regulatory clarity: businesses and banks may feel more confident integrating stablecoins into their operations without fear of sudden regulatory crackdowns.

A stablecoin-friendly approach boosts fintech, payments, and blockchain innovation.

Where’s Bridge in all this?

Bridge’s bet on the future of stablecoins

Bridge is built on two fundamental ideas:

Stablecoins will be very important

There will be many of them

While blockchain technology offers inherent advantages, it still requires simplification layers to make it accessible for mainstream businesses and users.

Bridge is solving this by doing what Stripe did 14 years ago when it revolutionised online payments with its famous “7 lines of code” to enable businesses to effortlessly accept card payments.

Now, Bridge is applying the same playbook to power the next wave of digital payments, making stablecoin transactions as seamless as traditional finance.

“I wouldn’t be surprised if stablecoins become the largest holders of U.S. Treasuries”

Zach Abrams, Bridge’s co-founder

What is Bridge and How Does It Work?

Bridge operates as a key infrastructure provider within the stablecoin ecosystem. Think of them as the builders of roads and bridges (hence the name) that connect different parts of the digital economy. Their core offerings revolve around:

Orchestration APIs: These APIs streamline the process of moving money between fiat currencies and various stablecoins. They provide a seamless and efficient way to convert currencies, manage transactions, and interact with different blockchain networks.

Issuance APIs: This technology allows businesses to easily create and issue their own stablecoins, tailored to their specific needs and use cases. This opens up new possibilities for loyalty programs, rewards systems, and digital currencies with specific functionalities.

Virtual Accounts: To allow countries outside of the US to establish a financial connection into the US.

Card Issuance API: For businesses that are trying to create cards.

Bridge provides the underlying technology that allows fintechs, digital banks, and other businesses to leverage the power of stablecoins for a variety of applications.

Bridge's Business Model

Bridge's business model is based on:

API Usage Fees: They generate revenue by charging fees for the usage of their APIs. As more transactions flow through their infrastructure, their revenue increases.

Card Issuance Revenue

Their business model aligns with their mission of creating a frictionless financial system.

Stripe’s acquisition

Last week, Stripe completed the acquisition of Bridge for $1.1 billion. This acquisition wasn't just a validation of Bridge's technology; it was a strategic move to solidify Stripe's position in the future of finance.

"We expected Bridge… to grow very quickly, and we're nevertheless shocked at just how rapidly adoption is exploding. In the coming years, everyone programmatically moving money will likely want a stablecoin strategy."

Stripe CEO - Patrick Collison

This acquisition provides Bridge with access to Stripe's vast resources, brand recognition, and network of customers, accelerating its growth and ability to shape the stablecoin ecosystem. It will allow them to scale their business, but also gives them credibility in the B2B space.

The Challenges

Despite their early success and strategic acquisition, Bridge still faces several challenges:

Regulation: stablecoins governance is still evolving. Bridge will need to stay agile and adapt to changing regulations globally.

Building trust and security: better confidence in stablecoins and their underlying technology is a must to become successful. Bridge initially hit a few blows on this front with multiple bank partnerships falling through.

Achieving interoperability: Ensuring seamless compatibility between different stablecoins and blockchain networks is crucial for creating a truly global financial system.

Opportunities for Fintechs & Digital Banks

Stablecoins offer the best of both worlds: the stability of traditional currencies with the efficiency of blockchain technology. As infrastructure for accessing, issuing, and using digital currencies matures, fintechs have a unique opportunity to build for the future, instead of simply patching outdated systems.

Here are some opportunities:

Cross-border payments: stablecoins can facilitate faster, cheaper, and more transparent cross-border payments compared to traditional methods. Fintechs can build remittance services or solutions for international businesses leveraging this advantage.

Increase financial inclusion: Digital banks can offer access to financial services to underserved populations who may not have access to traditional banking infrastructure.

New innovative products: stablecoins enable the creation of new financial products and services, such as tokenized assets, fractional ownership, and smart contract-based lending.

New revenue opportunities (i.e. bridge has provisioned what they call “developer fees” as part of their infrastructure).

Enable better loyalty programs

Stablecoin payment gateways & merchant solutions

Compliance & KYC solutions for stablecoins

B2B trade settlements & supply chain payments

Products for global travellers, tourists and digital nomads

Products for global freelancers & remote employees

New payroll and accounting products

New cross-border & niche digital banks (i.e. banks for digital nomads, expats etc)

Digital banks for AI agents

In just a few years, two major technologies, AI & blockchain, have evolved from white papers to real-world applications. We are now entering a new era where fintechs, AI, and Web3 projects can converge to create entirely new paradigms in finance and beyond.

Before the internet, we didn’t know we needed search engines - yet today, the global search market is worth $226.28 billion, and Google’s parent company, Alphabet, sits at a $2.266 trillion market cap.

Search is just one example of how new technologies enables products we couldn’t have imagined before.

Now, we stand at the beginning of a new financial era, with AI and blockchain as the foundation for innovation.

What will you build?

More on the subject here:

About Dom Monhardt, founder of one-fs.com

I am a French technologist and product leader living in Dubai, with 15+ years of experience in building cutting-edge and innovative digital experiences.

I am interested in the intersection of business, design, and technology and am deeply passionate about the fintech and digital banking world.

Excellent. Do you believe the rise of stablecoins will eat away at the dominance of Mastercard and visa?